Grain markets by the numbers

By Matt Wallis

Monday night the USDA released the August edition of the World Agricultural Supply and Demand report which painted an interesting picture for global grain markets. Following the release of the report, nearby CBOT contracts experienced sharp declines. Wheat closed to trade 28 USc/bu or $15AUD/t lower, corn 25 USc/bu or $14 AUD/t lower and soybeans 12.25 USc/bu or $7 Aud/t lower.

US wheat production and ending stocks were forecast to increase marginally while global production and ending stocks have been revised lower by 3.4 million mt and 1.06 million mt respectively. Offsetting the lower production is a reduction in global wheat demand of approximately 2 million mt however it is important to understand that where global production has been cut is Russia (1.2 million mt) and the European Union (1.3 million mt) which are both major wheat exporters. Russia is now projected to produce 73 million mt which is a far cry from the 80 million mt estimates that were floating around earlier this year.

All of this sounds great for producers and may generate arguments for a bullish global market, but the unfortunate reality is that the global S&D’s are still heavy with ending stocks projected at a record high of 285.40 million mt. To put this in perspective, this figure is 9.91 million mt higher then 2018/19 estimates and 4.22 million mt higher than 2017/18.

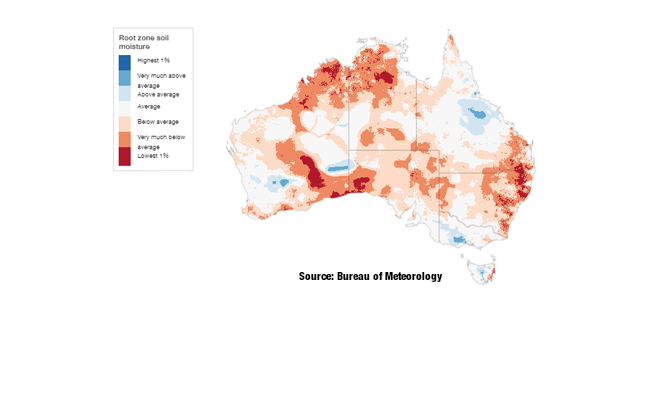

Moving onto Australia and the USDA has left our domestic wheat production unchanged at 21 million mt which is in line with ABARES latest forecast of 21.19 million mt. However, given the current environment one must ask whether this number is still achievable? The climatic conditions have been well documented on the eastern seaboard to date and the forecasts don’t appear to be in our favour for the time being. However we have learnt to take that with a pinch of salt. It is worth noting that the crop that is there is well backed by both NDVI data and growers who have expressed the potential of the coming harvest. To further refine the areas, southern NSW is set up well south of Barmedman and western areas around Merriwagga, Goolgowi and Tabbita are reported to be in the box seat to capture some handy cereal crops. Sub-soil moisture is no doubt the limiting factor here and we will need multiple widespread soaking rain events promptly if the potential is to be realised. Moving into Victoria and its quite difficult to find an area that drags the chain. The Wimmera, Mallee, Western Districts and Central Victoria are all reported to be in excellent condition and on track for a bumper season provided the spring is kinder than the last few years.

ABARES seems to support the Victorian conditions with state production estimates as follows: Wheat 3.2 million mt, Barley 1.8 million mt and Canola of 550k mt. If these estimates were to be realised today, they would account for 37% of wheat, 53% of barley and 51% of the canola on the east coast. If we were to look at the long-term forecast, it would be fair to assume that these percentages could have further potential to the upside.

In local markets we haven’t seen much of note lately. Old crop wheat delivered into Griffith has been bid at $360-$370 while new crop wheat has been bid at the same range in the Port Kembla Zone. Barley seems to have lost $10-$20/t of late trading around $360-$370 ex-farm in SNSW.

Grain Markets they are a changing

Does the East Coast market ever go back to a normal season? I guess that depends what you classify as a normal season! Needless to say, the landscape through our part of the grain belt has changed dramatically in recent times and will continue to do so.

Read MoreSentiment drying up fast

The week that has been saw 1-2mm fall sporadically across southern NSW with nothing registering to the north or west. The forecast isn’t showing any encouraging signs in the next week whilst the days are becoming longer and warmer.

Read MoreUSDA surprised the market when releasing their production and end stocks numbers in the monthly WASDE

Wheat futures were catapulted last week after the US Department of Agriculture (USDA) surprised the market when releasing their production and end stocks numbers in the monthly WASDE (World Supply and Demand Estimates) Report.

Read MoreNew Season Crop In Focus

It is still wet in the United States and most areas above Forbes in Central New South Wales are really feeling the pinch due to lack of any decent rainfall. We can only hope that there is a turn around soon in the season for everyone’s sake.

Read More